In today’s economic landscape, the US faces an uncomfortable truth: the expectation of a soft landing may not hold true. Recent economic history has taught us that complacency can be our worst enemy. And there are compelling reasons to believe that a recession might be closer than we think.

Despite lower inflation, robust job growth, and continued consumer spending, avoiding a recession is not guaranteed, even by the Fed. While a last-minute deal delayed a government shutdown, other factors could impact GDP growth in Q4, pushing the U.S. economy into recession.

Here are six compelling reasons why a recession remains the base case for Bloomberg Economics. Their factors cover everything from human behavior to labor strikes, rising oil prices, and a looming credit squeeze. These factors, combined with the end of Taylor Swift’s concert tour, create a complex economic landscape that demands attention.

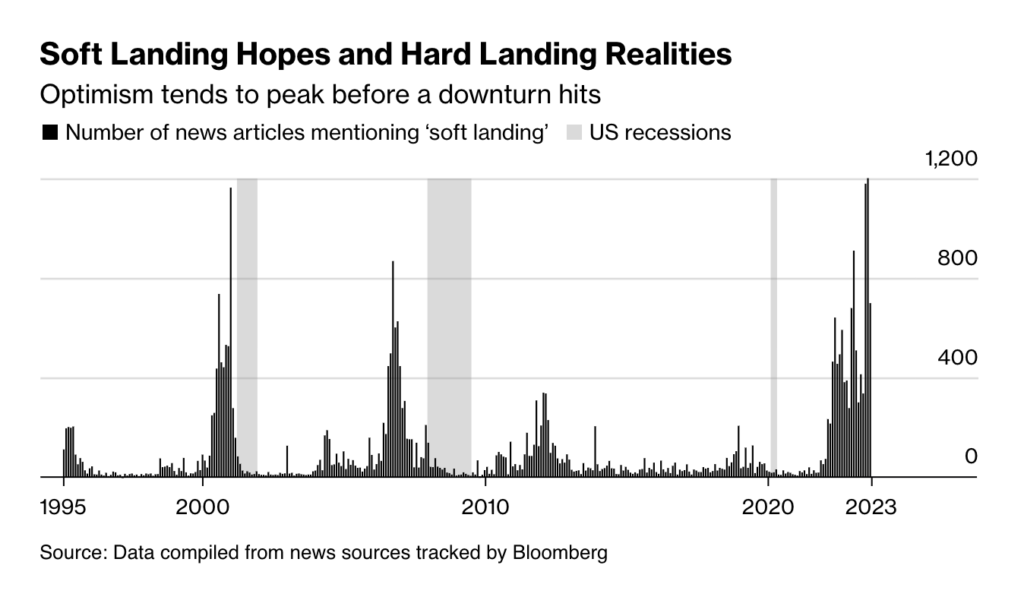

1. Historical Precedent: History and data reveal that the consensus has grown too complacent before every U.S. downturn over the past four decades. Soft landing predictions often precede economic hard landings.

2. Complex Forecasting: Economists face difficulties predicting recessions due to the nature of forecasting. Traditional forecasting relies on linear assumptions, while recessions are non-linear events, making them challenging to anticipate.

3. Unemployment Trends: The Federal Reserve’s forecast predicts a gradual increase in the jobless rate from 3.8% in 2023 to 4.1% in 2024, seemingly avoiding a recession. However, nonlinear shifts in economic trends can disrupt this pattern.

4. Skewed Risks: A non-linear approach to forecasting reveals that the risks of higher unemployment are disproportionately high, suggesting that the job market might not be as stable as it appears.

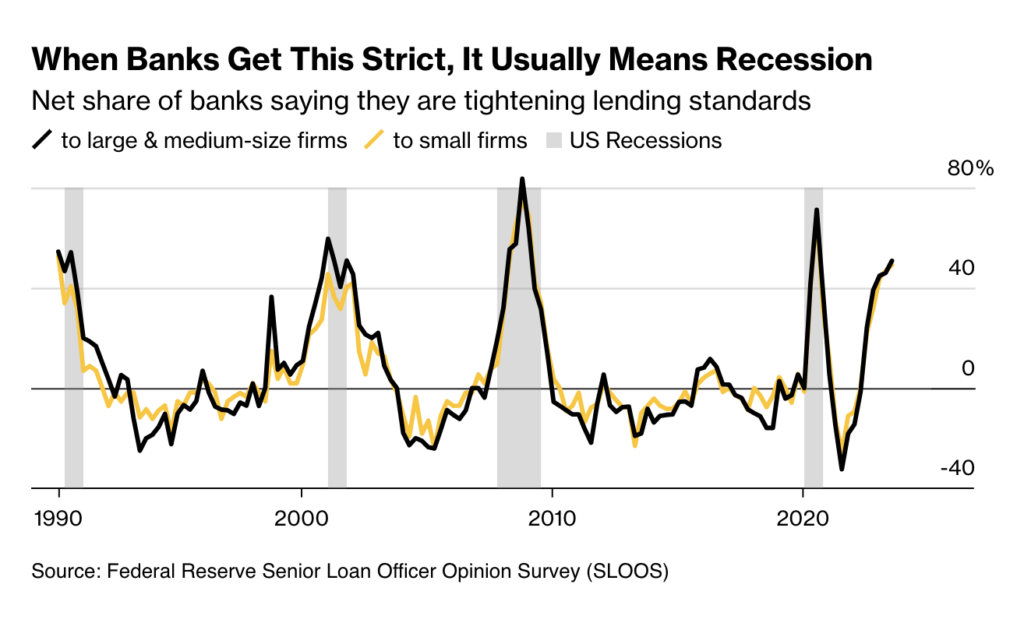

5. Monetary Policy Lag: As Milton Friedman famously noted, monetary policy operates with long and variable lags. The impact of interest rate hikes can vary across different sectors of the economy, and the effects may not be immediately evident. Banks aren’t lending much, and that usually forecasts a recession.

6. Short-Term Positives: While stock performance, manufacturing improvement, and a resurging housing market are positive indicators, these areas have shorter lag times from rate hikes to real-world consequences. Consequently, their current strength may not be indicative of the broader economic landscape.

That’s Before These Shocks Could Cause a US Recession

That assessment is mostly based on forecasts delivered over the past few weeks — which might not capture some new threats that are threatening to knock the economy off course. Among them:

–Auto Strike: The United Auto Workers union has called a walkout at America’s Big Three auto firms, the first time they’ve all been targeted at the same time. It expanded the strike on Friday to encompass some 25,000 workers. The industry’s long supply chains means stoppages can have an outsize impact. In 1998, a 54-day strike of 9,200 workers at GM triggered a 150,000 drop in employment.

–Student Bills: Millions of Americans will start getting student-loan bills again this month, after the 3 1/2-year pandemic freeze expired. The resumption of payments could shave off another 0.2-0.3% from annualized growth in the fourth quarter.

–Oil Spike: A surge in crude prices — hitting every household in the pocket book — is one of the handful of truly reliable indicators that a downturn is coming. Oil prices have climbed nearly $25 from their summer lows, pushing above $95 a barrel.

–Yield Curve: A September selloff pushed the yield on 10-year Treasuries to a 16-year high of 4.6%. Higher-for-longer borrowing costs have already tipped equity markets into decline. They could also put the housing recovery at risk and deter companies from investing.

–Global Slump: The rest of the world could drag the US down. The second-biggest economy, China, is mired in a real-estate crisis. In the euro area, lending is contracting at a faster pace than in the nadir of the sovereign debt crisis — a sign that already-stagnant growth is set to move lower.

–Government Shutdown: A deal to keep the government open has kicked one risk from October into November – a point where it could end up doing more damage. Bloomberg Economics estimates that each week of shutdown takes about 0.2 percentage point off annualized GDP.

In conclusion, the U.S. economy stands at a crossroads. With multiple factors converging, that suggests a recession could be imminent. History and data indicate that soft landings often precede hard landings. Economists must grapple with the challenge of forecasting non-linear economic events. With various risks on the horizon, it is crucial to exercise caution and remain vigilant. The addition of these new threats only underscores the need for careful monitoring and proactive measures to safeguard the economy.

Recent Posts

-

Capital Financing for the Micro and Lower Middle MarketSeptember 28, 2025

Capital Financing for the Micro and Lower Middle MarketSeptember 28, 2025 -

Sales Based Financing for the Micro and Lower Middle MarketSeptember 22, 2025

Sales Based Financing for the Micro and Lower Middle MarketSeptember 22, 2025 -

SBA Business Loans: A Blueprint for Growth and SuccessAugust 15, 2025

SBA Business Loans: A Blueprint for Growth and SuccessAugust 15, 2025 -

Structured Capital: Strategic Financing for Growth and StabilityAugust 15, 2025

Structured Capital: Strategic Financing for Growth and StabilityAugust 15, 2025 -

How Net Working Capital Can Make or Break Your BusinessJuly 18, 2025

How Net Working Capital Can Make or Break Your BusinessJuly 18, 2025