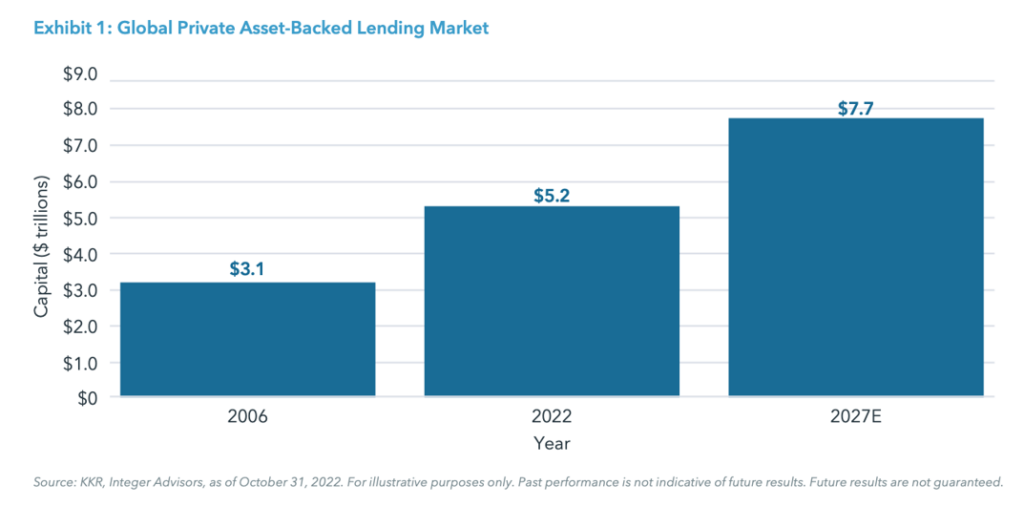

In the realm of financing, asset-based lending (ABL) stands out as a robust option. Set to be a $1.72T market by 2031 – with some estimates as high as $7.7T – ABL offers businesses with a sizable balance sheet the ability to access funds by leveraging assets. In general, ABL financing leverages assets like accounts receivable, inventory, equipment, and real estate to secure a loan. ABL can be tailored to a certain asset class, which would likely require agreement among numerous lenders via an inter-creditor agreement. This type of financing is ideal, because it’s affordable, secured by assets, and offers the necessary capital required for any business use.

Contents

Understanding Asset-Based Lending

At its core, asset-based lending is tailored for businesses that possess substantial assets but might lack the liquidity when needed. Funds can be used for refinancing existing debt, settling debts with vendors, operational improvements, or general working capital. This form of financing hinges on collateralizing assets to secure a line of credit or loan, offering a safety net for both the borrower and the lender.

Qualifying Factors and Underwriting Process

For businesses eyeing asset-based lending, having certain assets is key. Lenders typically assess the quality, value, and liquidity of these assets as part of the underwriting process. The evaluation delves into the strength of the assets and the borrower’s ability to repay the loan. While creditworthiness is considered, the primary focus remains on the collateral offered. In general, the more liquid assets get a higher loan-to-value (or advance) rate, whereas the more illiquid assets get a lower “advance” rate.

Qualifying Assets: A Diverse Range

Asset-based lending encompasses an array of assets that businesses can leverage to obtain financing. Beginning in the upper left hand corner of the balance sheet:

Accounts Receivable (A/R)

This includes outstanding customer invoices, representing a considerable portion of a company’s current assets. Lenders evaluate the quality and aging of receivables to determine their eligibility for financing. Given the short-term nature of the asset class, and provided the credit quality of the payor is good, lenders can offer up to 90% against the stated invoice value.

Inventory

Businesses can use their inventory, such as raw materials, work-in-progress goods, or finished products, as collateral. The valuation and marketability of inventory are pivotal in determining its financing potential. Given that inventory is less liquid than A/R, the advance rate is less, generally around 60%. Lenders won’t lend to work-in-progress inventory, but will lend to finished goods inventory.

Machinery and Equipment

Tangible assets like machinery, equipment, and vehicles can also serve as collateral. Their condition, market value, and depreciation play a crucial role in the lending decision.

Real Estate

Properties owned by the business, whether office buildings, manufacturing facilities, or land holdings, can be utilized to secure loans. The location, market value, and potential for appreciation factor into their financing viability.

Potential Hurdles to Asset Based Lending Deals

Despite its advantages, asset-based lending isn’t without potential obstacles. Most commonly, businesses have one lender that takes security in multiple assets. For example your bank might be “super senior” on inventory, receivables, and machinery. And if the business needs additional capital, there might be a specialized inventory lender that can finance that asset. In which case, the bank will have to agree to “carve out” that asset so the business can finance it. Obtaining collateral carve out of assets to finance (i.e. receivables) is a major challenge for businesses with a “super senior” lender on all assets. The only other options then are equity or unsecured financing, which are far more expensive than ABL.

With a properly structured ABL facility, a business should only offer up as security the asset which is being financed. If the lender is not OK with being “super senior” on that asset, then they are not an asset based lender; they are just a business lender.

The Loan-To-Value Ratio (LTV%) and Borrowing Base Calculations

As mentioned, businesses can finance an array of assets, including accounts receivable, inventory, machinery, equipment, and real estate. The Loan-to-Value (LTV) ratio and borrowing base are fundamental metrics in this domain. The LTV ratio assesses the loan amount as a percentage of the appraised asset value, while the borrowing base calculates the maximum amount a borrower can obtain against that value.

Empowering Businesses with Asset Based Lending

In the landscape of asset-based lending, Babylon Asset Management stands out as a guiding force. We offer tailored financial solutions for businesses with annual sales ranging from $1M to $50M. Leveraging extensive experience and expertise, Babylon Asset Management aids businesses in navigating the complexities of asset-based capital.

By understanding the unique needs of each business, Babylon Asset Management facilitates access to flexible capital, enabling growth, operational agility, and enhanced financial stability. Through meticulous assessment and a customer-centric approach, they ensure businesses capitalize on their assets to secure the funding they need.

Recent Posts

-

Capital Financing for the Micro and Lower Middle MarketSeptember 28, 2025

Capital Financing for the Micro and Lower Middle MarketSeptember 28, 2025 -

Sales Based Financing for the Micro and Lower Middle MarketSeptember 22, 2025

Sales Based Financing for the Micro and Lower Middle MarketSeptember 22, 2025 -

Structured Capital: Strategic Financing for Growth and StabilityAugust 15, 2025

Structured Capital: Strategic Financing for Growth and StabilityAugust 15, 2025 -

How Net Working Capital Can Make or Break Your BusinessJuly 18, 2025

How Net Working Capital Can Make or Break Your BusinessJuly 18, 2025 -

What Is a Business Capital Loan and Why They MatterJuly 16, 2025

What Is a Business Capital Loan and Why They MatterJuly 16, 2025