Almost two weeks ago, we got an outsized GDP reading of over 3%. Last week we expected 185,000 new jobs, we got 300,000+. The market continued to rally, despite the fact that higher for longer might be on the table again. Then on Sunday’s 60-Minutes interview with Chairman Powell, he noted that a rate cut by March is unrealistic.

This sent shivers were sent through the markets – from bonds to oil – except in equities, where technology continues to drag stocks higher. Knockout earnings from Facebook, Nivida, and others, are defying interest rates. Meanwhile 10-year yields rocketed from 3.86% to over 4.11 since The FOMC meeting last Wednesday.

The winds of change are blowing through the financial markets, and investors are feeling the chill. The recent Federal Open Market Committee (FOMC) meeting and Powell’s interview on 60 Minutes last night has left a distinct imprint on market sentiment, signaling a departure from the earlier anticipation of an interest rate cut as soon as March (!). The resounding consensus? “Higher for longer” is back on the table, and this unexpected turn has sent shivers down the spines of investors worldwide, except of course – equities.

Contents

- 1 Market Expectations Take a Turn

- 2 Economic Data Paints a Different Picture

- 3 Sticky Core Inflation: The Thorn in the Fed’s Side

- 4 Misinterpreting Powell’s Signal of Higher for Longer

- 5 New Faces, New Perspectives

- 6 A Divided Committee on Higher for Longer

- 7 Balancing Act: The Fed’s Dilemma

- 8 Higher for Longer: How High, and How Long?

Market Expectations Take a Turn

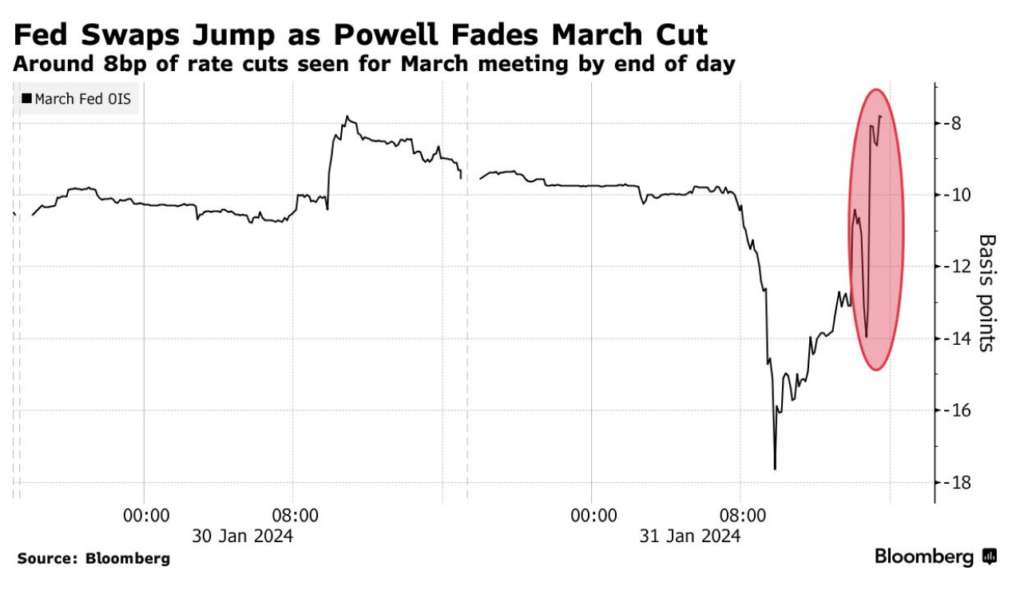

In the aftermath of the first FOMC meeting of 2024, the markets have swiftly revised their expectations. A mere 34% now anticipate an interest rate cut in the upcoming March meeting, a significant drop from the 73% consensus just one month ago. The abrupt shift in market sentiment suggests that the much-discussed “higher for longer” scenario is gaining traction, catching investors off guard.

Economic Data Paints a Different Picture

Diving into the economic landscape, the data paints a picture that doesn’t align with the earlier expectations of a rate cut. Inflation, a key metric, surprised the market by coming in higher than anticipated in December. The labor market remains as tight as ever, with an ultra-low unemployment rate of 3.7%. Retail sales defied projections, rising more than expected last month, even though some of it can be attributed to the festive season.

Looking ahead, while the annual January blues might drive inflation and spending lower temporarily, there is an expectation of a rebound later in the quarter. The overarching narrative is clear – the economy is still running hot. It is the economic data that serves as the compass for the FOMC’s monetary policy decisions.

Sticky Core Inflation: The Thorn in the Fed’s Side

A key player in this unfolding drama is core inflation, the Federal Reserve’s preferred measure. December saw an unexpected rise in both month-over-month (MoM) and year-over-year (YoY) core inflation. The data reveals that inflationary pressures have primarily stemmed from the services sector, exacerbated by the tight labor market.

Despite talks of a potential softening in labor conditions, the unemployment rate in December remained at an enviable 3.7%. Initial jobless claims, a leading indicator, have averaged well below historical norms in recent weeks. Wage growth, a significant factor in the inflation equation, accelerated to 6.5% YoY in November. The combination of higher wages, increased credit spending, and robust consumer sentiment fueled a surge in U.S. retail sales, beating analysts’ expectations.

Misinterpreting Powell’s Signal of Higher for Longer

The market, it seems, may have misinterpreted signals from Fed Chairman Jerome Powell. While Powell acknowledged the possibility of a discussion on rate cuts “coming into view,” he consistently emphasized that the primary objective remains the 2% inflation target, even if it means enduring an economic slowdown. Powell’s rhetoric throughout much of 2023 was more hawkish than credited by the market, and recent statements suggest a softening, but not an abandonment, of this stance. However, with a hot GDP, employment report, and comments that a cut is not happening any time soon – he squarely put “higher for longer” back on the table.

New Faces, New Perspectives

The changing of the guard at the FOMC in 2024 introduces new perspectives that could contribute to a more hawkish stance. Among the four incoming members, only San Francisco Fed President Mary Daly has publicly advocated for a discussion on rate cuts. Richmond Fed President Tom Barkin desires further declines in inflation, Atlanta’s Raphael Bostic foresees cuts in the second half of the year, and Cleveland’s Loretta Mester believes market expectations have outpaced the Fed’s intentions.

A Divided Committee on Higher for Longer

As the FOMC faces a year of more contentious monetary policy decisions, the potential for a more divided committee looms large. This internal divergence could further delay any interest rate cuts, adding complexity to an already delicate situation.

Balancing Act: The Fed’s Dilemma

The Fed finds itself in a delicate balancing act after a challenging 2023. While victory in the battle against inflation appears within reach, the economic landscape remains unpredictable. Several factors, including geopolitical unrest, could push inflation higher. Conversely, the effects of monetary tightening take time to materialize, potentially leading to an economic slowdown.

As the economy continues to show strength and the specter of persistent inflation persists, the Fed is likely to maintain a cautious stance on interest rates. Even when core inflation eventually recedes toward the 2% target, the article suggests that the aggressive cutting cycle predicted by many pundits may not materialize. Brace yourselves – “higher for longer” rates are here to stay, and it’s time for the market to adjust to this new paradigm.

Higher for Longer: How High, and How Long?

In the wake of the recent FOMC meeting, the financial markets are grappling with a shift in expectations. The resurgence of the “higher for longer” scenario has spooked investors, challenging earlier assumptions of an imminent interest rate cut. It appears now that the only way a cut is happening is if there is a big enough spook that could freeze up credit markets. As economic data continues to shape the narrative, the Fed faces a complex task of balancing its dual mandate amidst a changing of the guard and potential internal divisions. The road ahead is uncertain, and investors must navigate carefully through the evolving landscape of monetary policy. Yields are still somewhat inverted, so therefore we are paying attention very closely.

Recent Posts

-

Capital Financing for the Micro and Lower Middle MarketSeptember 28, 2025

Capital Financing for the Micro and Lower Middle MarketSeptember 28, 2025 -

Sales Based Financing for the Micro and Lower Middle MarketSeptember 22, 2025

Sales Based Financing for the Micro and Lower Middle MarketSeptember 22, 2025 -

Structured Capital: Strategic Financing for Growth and StabilityAugust 15, 2025

Structured Capital: Strategic Financing for Growth and StabilityAugust 15, 2025 -

How Net Working Capital Can Make or Break Your BusinessJuly 18, 2025

How Net Working Capital Can Make or Break Your BusinessJuly 18, 2025 -

What Is a Business Capital Loan and Why They MatterJuly 16, 2025

What Is a Business Capital Loan and Why They MatterJuly 16, 2025